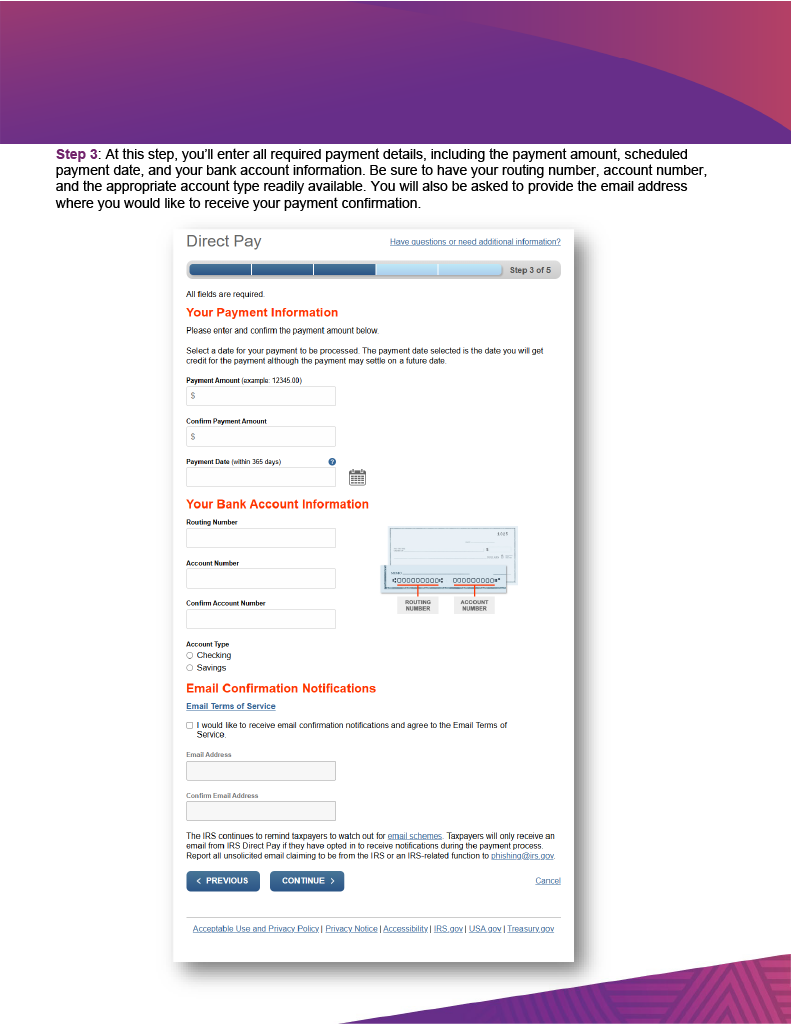

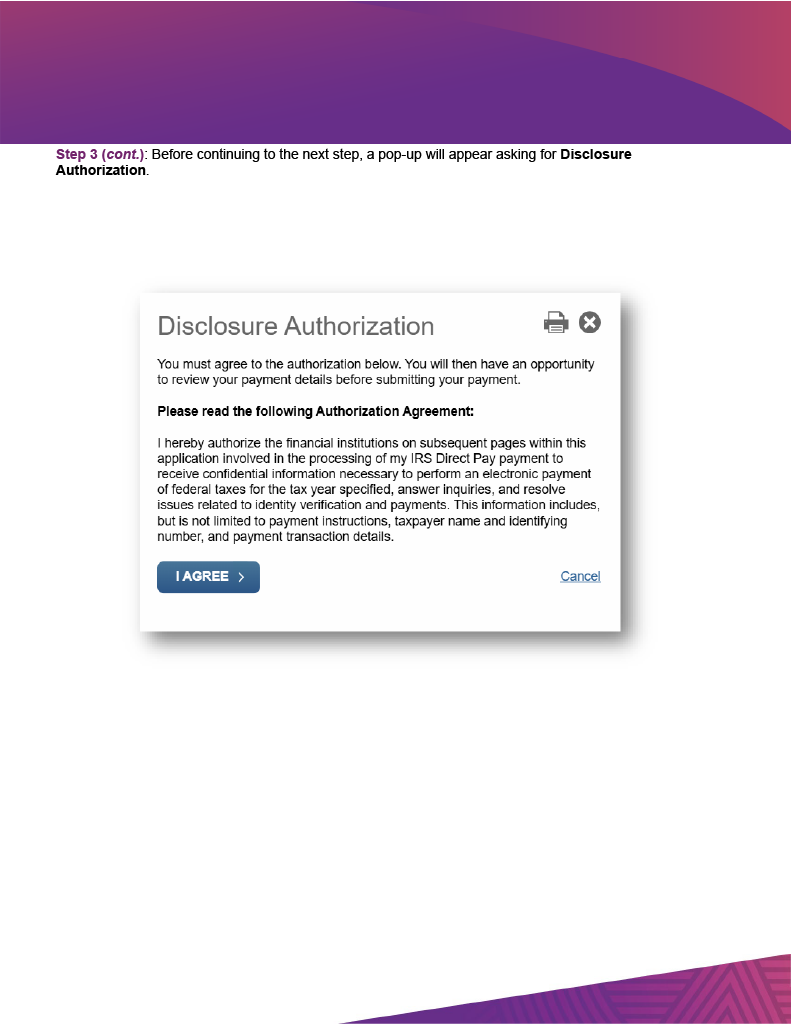

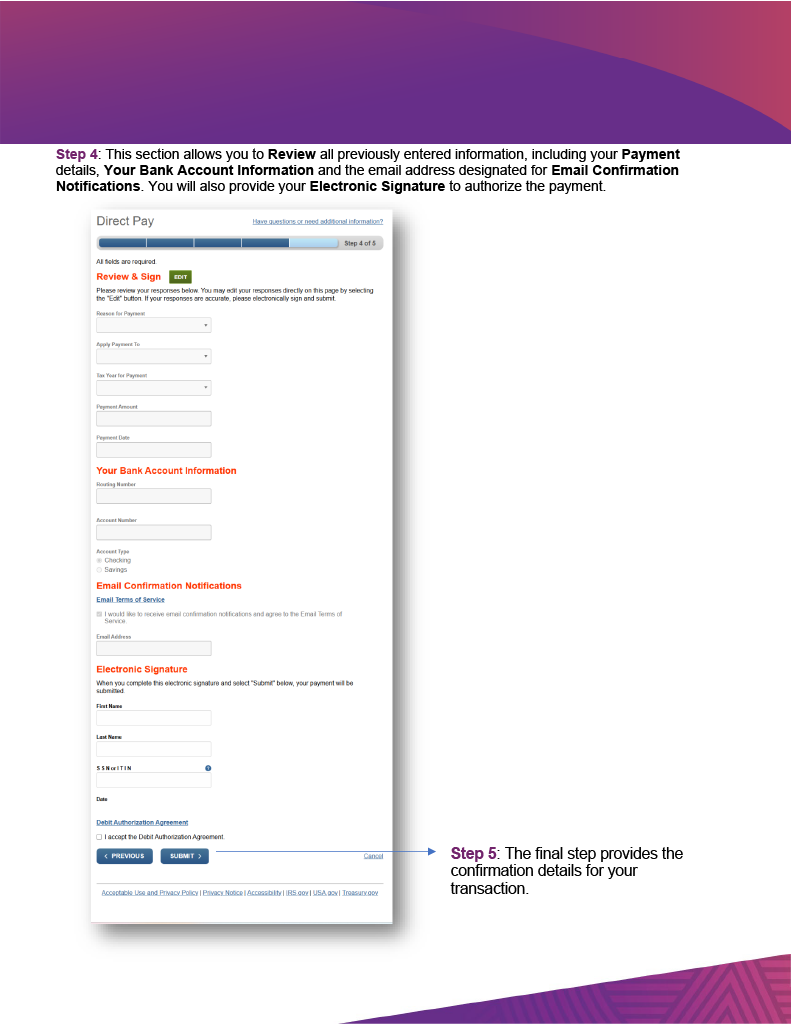

The SECURE 2.0 Act of 2022 (Act) was signed into law on December 29, 2022, to increase retirement savings, improve retirement rules, and lower employer costs of setting up a retirement plan. Plan amendments required by the Act generally need not be made until the end of the first plan year beginning on or after January 1, 2025; however, plans must be operated in accordance with the effective date of each new provision. Following is a summary of some of the significant provisions that may affect plan sponsors and auditors:

Autoenrollment/auto escalation: Effective for plan years beginning after December 31, 2024, new 401(k) and 403(b) plans must automatically enroll participants when they become eligible; employees may opt out of coverage. All 401(k) and 403(b) plans in effect on the date of enactment are grandfathered; small businesses with 10 or fewer employees, new businesses (i.e., those that have been in business for less than three years), church plans, and governmental plans are exempted from this provision.

Repeal and replacement of the Saver’s Credit: A new “Saver’s Match” will replace the current law nonrefundable “Saver’s Credit” for certain individuals who make contributions to employer retirement plans. The match is subject to an income-based phase out and becomes effective for tax years beginning after 2026.

Required Minimum Distributions (RMDs): The RMD age will increase in 2023 and again in 2033. Starting in 2024, Roth accounts will be exempt from the RMD rules while the participant is alive.

Catch-up contributions: The catch-up contribution limit will increase for taxable years beginning after December 31, 2024. Starting in 2024, all catch-up contributions must be Roth contributions for participants with compensation equal to or in excess of $145,000.

Changes to long-term, part-time employees: The Act modifies the measuring period for long-term, part-time employees from three years to two years and also extends the long-term, part-time employee provision to 403(b) plans that are subject to ERISA.

Student loan payments: For plan years beginning after December 31, 2023, employers may make matching contributions under a 401(k) or 403(b) plan on employees’ qualified student loan payments. Employees who receive such matching contributions are required to certify annually to the employer that such payment has been made on such loan.

Withdrawals for certain emergency expenses: The Act provides an exception from the 10% tax on certain early distributions made after 2023 that are used for emergency expenses which are unforeseeable or immediate family needs relating to personal or family emergency expense. Plan administrators generally may rely upon a participant’s self-certification; however, the IRS is authorized to issue guidance to address situations in which a plan administrator has actual knowledge to the contrary or there are employee misrepresentations.

Increased dollar threshold for mandatory distributions: For distributions after December 31, 2023, the involuntary distribution threshold will increase from $5,000 to $7,000.

Pension linked emergency savings accounts (ESA): Beginning in 2024, DC plans may include an ESA for non-highly compensated employees; accounts are part of the plan document but accounted for separately. Employers may automatically opt their employees into these accounts, and all contributions must be made on an after-tax basis.

Recovery of retirement plan overpayments: Effective immediately, retirement plan fiduciaries have the discretion to not recoup overpayments mistakenly made to retirees. Where a plan’s fiduciaries choose to recoup overpayments, collection efforts are subject to certain limitations and protections to safeguard retirees. Rollovers of the overpayments remain valid.

Compliance testing/corrections: The Act includes changes to the rules for top-heavy plan testing, expands the IRS Employee Plans Compliance Resolution System to allow more types of errors to be rectified internally through self-correction and exempt certain failures to make RMDs from the excise tax penalty, and allows for a grace period to correct, without penalty, reasonable errors in administering automatic enrollment and automatic escalation features occurring after December 31, 2023.

403(b) plans: The Act conforms the current hardship distribution rules for 401(k) plans to 403(b) plans and the long-term, part-time employee provision is extended to 403(b) plans that are subject to ERISA. In addition, 403(b) plans will now be allowed to invest in collective investment trusts (CITs). Beginning in 2023, 403(b) plans can join a multiple employer plan (MEP) or pooled employer plan (PEP).

Annual audits for groups of plans: The Act clarifies that each plan filing under a group of plans (added by the SECURE Act) is required to submit audited financial statements if it has 100 participants or more. Plans with fewer than 100 participants that are included in a group of plans are not required to submit audited financial statements.

Other: The Act amends qualified birth and adoption distribution rules, permits plans to distribute money to pay premiums for high-quality long-term care insurance products and allow withdrawals by participants who have experienced domestic abuse.

Source: AICPA Employee Benefit Plans Audit Quality Center. Click here to read the SECURE 2.0 Act (included as Division T on pages 2,046 to 2,404 of the Consolidated Appropriations Act, 2023).

Contractors by their nature and occupation have a need to be in control. Nearly every project includes a struggle to maintain control of costs, safety and quality.

Contractors by their nature and occupation have a need to be in control. Nearly every project includes a struggle to maintain control of costs, safety and quality.